Find the right cover to take care of what matters most to you.

Our life insurance products

For Individuals

For Business

What is the difference between Variable age-stepped, Variable and Optimum premiums?

Understanding these premium types could help you better manage the cost of your insurance.

Understanding these premium types could help you better manage the cost of your insurance.

Understanding premiums and cover

Frequently Asked Questions

This is when your Total & Permanent Disablement (TPD) Cover or Crisis Recovery/Trauma Cover converts to protect you solely for Loss of Independence/loss of independent existence on the policy anniversary before you turn either 65 or 70.

Loss of Independence/loss of independent existence cover is less comprehensive and the policy terms are much more difficult to meet, compared to TPD Cover and Crisis Recovery/Trauma Cover.

Once your TPD or Crisis Recovery/Trauma cover has converted, you will only be paid a Loss of Independence/loss of independent existence benefit if you meet the definition of Loss of Independence/Loss of independent existence.

To fully understand the conversion of your cover to Loss of Independence and when this happens, it’s important for you to read and understand your policy document and any significant event notices we’ve sent you.

You can also learn more at conversion to loss of independence.

There are different ways you can structure your insurance protection when consulting with a financial adviser.

Depending on what suits your needs, budget, and personal circumstances, you can structure your insurance cover as:

- Stand Alone cover

- Rider cover, or

- Linked.

If you have Stand Alone cover, your cover will not be reduced after a claim payment under your other cover. For example, Chloe has Life Cover of $500,000 and Stand Alone Crisis/Trauma Cover of $200,000. When we pay Chloe the $200,000 Crisis/Trauma cover benefit, her $500,000 Life Cover remains the same.

However, if you have Rider Cover or Linked benefits, your cover will be reduced after a claim payment on your other cover. For example, Olivia has Life Cover of $500,000 and Rider Crisis/Trauma Cover of $200,000. When we pay Olivia the full Crisis/ Trauma benefit of $200,000, her Life cover is reduced to $300,000.

As life happens, your insurance needs may change. Major life events like marriage, career changes, growing your family, starting a business, or retiring may require a change in the amount, type, and structure of your insurance protection. We recommend that you regularly consult with your financial adviser to help you determine which options best suit your current circumstances.

You can also learn more about policy structure at understanding policy structure.

As policy owner(s) of a life insurance policy, you can nominate your preferred beneficiary/beneficiaries to receive financial support in the event of your death. This process is called nomination of beneficiaries.

For policies held outside super, the beneficiary/beneficiaries can be any person or entity like a family member, a company, or a trustee of a trust. Once a valid nomination is made, the death benefits will be paid directly to the nominated beneficiary/beneficiaries.

For policies held inside super, only the following beneficiary/beneficiaries are eligible under superannuation laws:

- your spouse (including your legally married spouse, de facto spouse, or same sex partner)

- your child/children (of any age) within the meaning of the Family Law Act 1975

- any person financially dependent on you

- a person in an interdependency relationship with you, or

- your Legal Personal Representative.

There are three types of nomination of beneficiaries for policies held inside super:

- Binding nomination – A legal binding nomination that is valid for three years and binds the trustee to distribute your death benefits as instructed by you in the nomination form. You need to review your nomination every three years before it expires.

- Non-lapsing binding nomination – A legal binding nomination that will continue to be valid until the expiry of your cover unless a new valid nomination is made or if the existing nomination is revoked.

- Non-binding nomination – A nomination made to the trustee that is non-binding. The trustee will consider your nomination, along with all other available information, but has discretion to decide how to distribute your death benefits.

If you do not make a nomination or if your nomination becomes invalid, it can result in a lengthy process before the death benefits can be paid. Even then, the money might not go to your intended beneficiary/beneficiaries.

It is important to review your nomination regularly to make sure it is still appropriate. We recommend obtaining expert financial or legal advice on the matter.

Learn more about nomination of beneficiaries at nomination of beneficiaries.

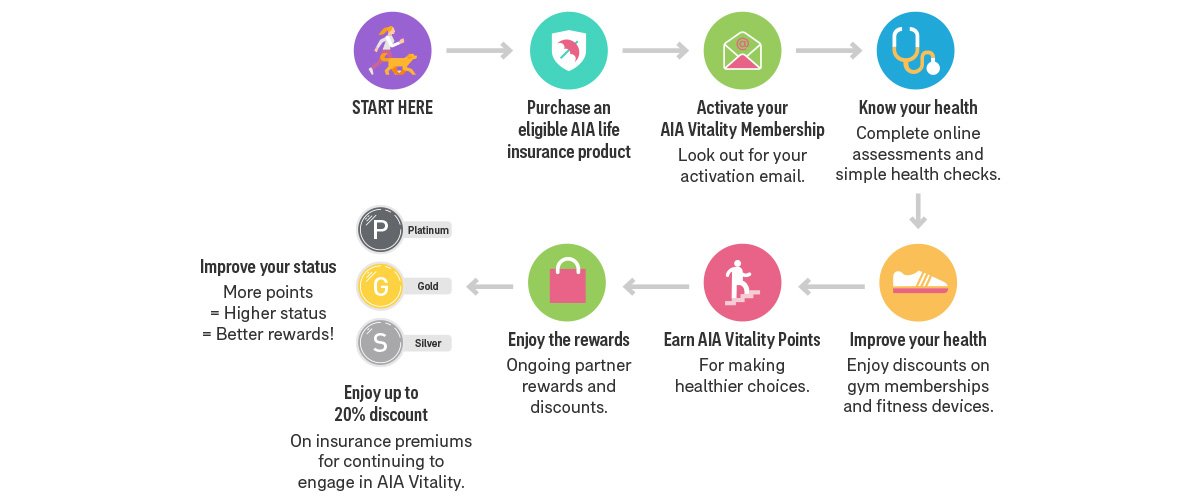

Life Insurance with AIA Vitality

The more you do to improve your health, the greater the rewards. You can attach an AIA Vitality membership to your life insurance or income protection cover to help you protect your most precious asset – your health.

Claims made easy

AIA Australia paid over $2.3 billion in total claims paid to customers during 2023, across our Retail, Group and Direct insurance policies.

Our priority is to support you through the claims process, ensuring that you understand what's happening every step of the way and that you get what you need as soon as possible.

Find out more

The more you do to improve your health, the greater the rewards. You can attach an AIA Vitality membership to your life insurance or income protection cover to help you protect your most precious asset – your health.

AIA Vitality content hub

Whether it’s your first foray into fitness or your gruelling third month of marathon training, AIA Vitality's Content Hub is your ultimate support team. Get the information and guidance you need to move well, think well, eat well and plan well. Your questions answered, inspirational stories and science-backed advice.